What Trade Business Owners Told Us About Succession Planning

Most trade business owners have thought about their exit. Few understand their real options. Here’s an honest breakdown of the five paths — and what each one actually means for a specialty contractor.

Table Of Contents

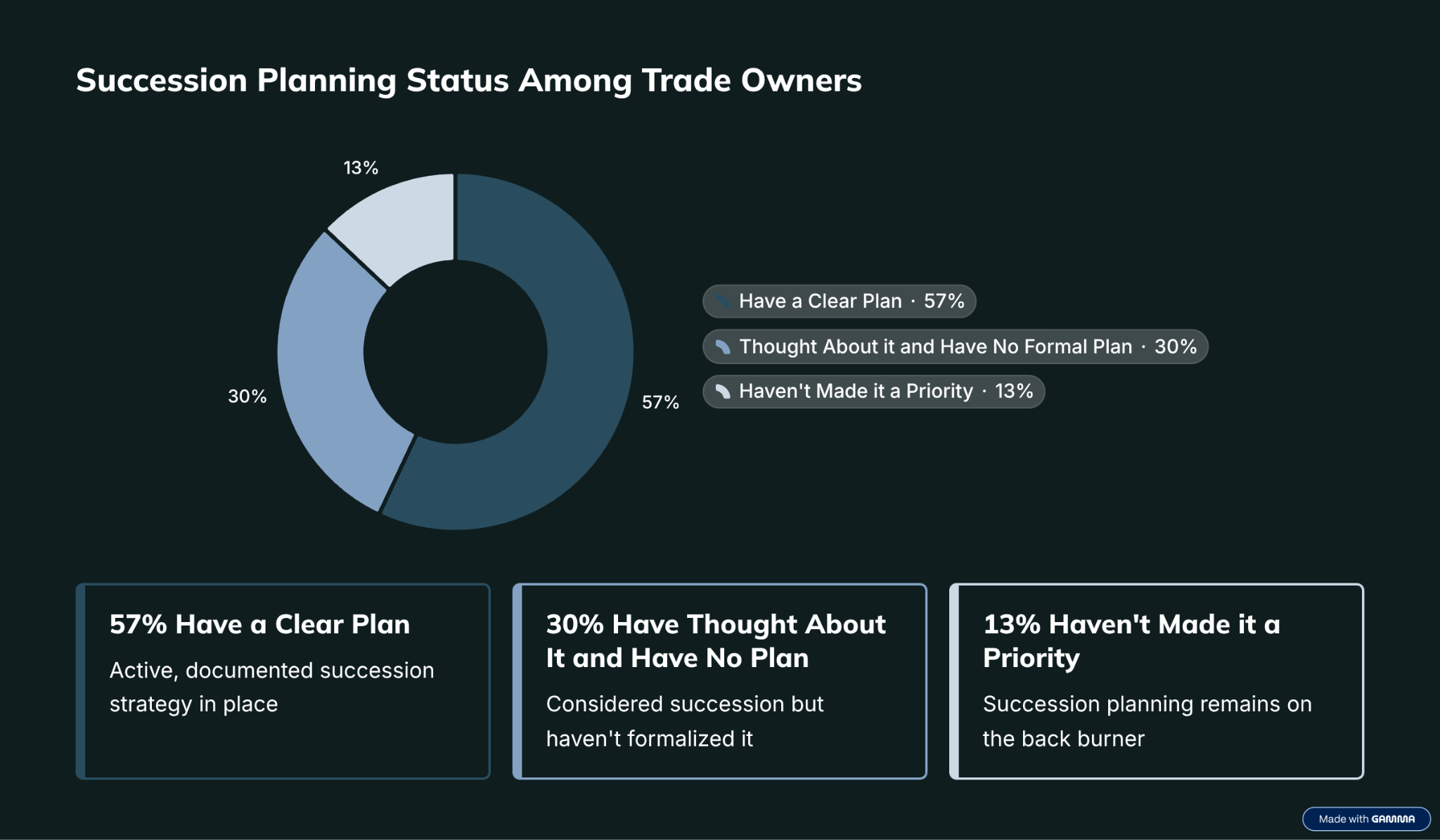

RiffleCM surveyed 200 trade business owners on succession planning — where they stood, what they understood, and what was stopping them from moving forward. 87% had at least thought about succession. Only 57% had a clear plan. Another 13% hadn't made it a priority at all. 34% expected to exit within the next five years.

That gap between awareness and readiness — nearly thirty points — is where most of the interesting data lives.

The Knowledge Gap Is Sharper Than the Planning Gap

The survey asked owners two related questions about five exit options: whether they had considered each one, and whether they understood it well enough to actually evaluate it. The distance between those two numbers tells a more specific story than the planning gap alone.

Management buyouts show the largest gap: 53% had considered one, but only 41% said they understood it well enough to assess. ESOPs sit close behind — 25% considered, 23% can evaluate — notable because it's the option with the most significant potential tax advantages and the most owner-friendly structure in terms of culture preservation. Wind-down is roughly even. Family succession is the one path where consideration and comprehension have kept pace: 54% considered it, 55% can evaluate it. Private equity is the outlier in the other direction — only 18% had actively considered it, but 30% said they could evaluate it. The market is educating owners about PE faster than they're choosing to pursue it.

These are not edge cases. The majority of owners in the survey — across all five paths — are carrying awareness without the understanding needed to make a real decision.

What the Broader Data Adds

The RiffleCM findings don't exist in a vacuum. FMI and CFMA's ownership transition research found that 58% of contractors lack any transition plan, and half of those planning to retire within three to five years have nothing in place. The Exit Planning Institute puts forced exits — death, disability, distress, disagreement, or divorce — at roughly 50% of all business exits.

Construction M&A data reinforces the urgency from the outside. Capstone Partners reported 562 construction transactions in 2025, up 18.2% year over year. For the first time, private equity buyers represented the majority of that activity — 54.3% of deals, according to Transjovan Capital. That number connects directly to the RiffleCM survey: 70% of trade business owners said PE consolidation was increasing in their market. The market is moving, and most owners are watching it without a plan that accounts for it.

Why Succession Planning Stalls: The Structural Problem

The survey included a question about what was stopping owners who hadn't made more progress. The most-cited response was financial dependence on the business. Roughly 40% of that group named it.

That finding describes two problems at once rather than just one.

The first is the retirement savings gap. For many trade contractors in the $1M–$5M revenue range, the business has been the primary financial instrument for a long time — not by design, but by default. Fidelity's 2023 Small Business Retirement Index found that 42% of self-employed and microbusiness owners worried they would never be able to retire. SCORE data shows 34% of small business owners have no retirement savings plan for themselves, and 18% plan to sell the business to fund retirement. WealthRabbit's 2025 Small Business Retirement Report found that the most common retirement savings amount among entrepreneurs aged 45 to 55 was $50,000, compared to average 401(k) balances of $152,000 to $199,000 for their corporate peers in the same age range.

The second problem is owner dependency and it's connected to the first. A business built around the owner's personal involvement has a fundamental valuation problem: buyers pay for a business that can generate cash after the seller leaves. Marcum LLP analysis puts the historical third-party sale success rate for construction companies at less than 25%. Owner dependency is among the most commonly cited reasons construction deals don't close.

The RiffleCM survey adds a specific dimension to this. When owners were asked what makes a business most valuable to a buyer, 53% named consistent revenue growth and profitability. But only 31% named a strong management team that can operate without the owner, and only 12% named well-documented processes. Those two factors — management depth and documented processes — are among the things buyers weigh most heavily in construction transactions. The gap between what owners think matters and what buyers actually pay for is part of what makes preparation so difficult to start.

Only 31% of owners in the RiffleCM survey had a formal valuation in the last three years. Another 19% said they had little idea what a buyer would pay.

These two problems compound each other. The business can't be sold for what the owner needs because the owner is what makes it work. And the owner can't afford to fix that because the business is the only income source. It is a self-reinforcing condition — not a failure of effort or ambition, but what tends to happen when a business owner's attention is spent on running the business rather than building the conditions for eventually leaving it.

What the Exit Options Actually Look Like

The RiffleCM survey data helps characterize each exit option not just in the abstract, but in terms of how prepared the industry actually is to pursue them.

Family succession is the most considered and the best understood of the five paths, but the nuance matters. It is still a financial transaction: the retiring owner needs liquidity, either from the business paying them out over time or the incoming family member taking on financing. Construction adds a bonding complication — sureties will evaluate a new owner from scratch, regardless of family history. Among owners considering family succession in the RiffleCM survey, 58% were confident the family member was ready, but 36% said the person was involved and needed more development time.

Management buyouts had the second-largest consideration gap — 53% considered, 41% can evaluate. The appeal is continuity. The challenge is almost always financing: most management teams don't have the capital, so deals require a mix of bank debt, SBA financing, and seller notes. Seller notes mean the owner's retirement money depends on a company they no longer fully control. An MBO is built over years, not assembled at the last minute.

ESOPs carry the sharpest knowledge gap in the data — 25% considered, 23% can evaluate — which is notable given the tax advantages available. A 100% ESOP-owned S corporation generally pays no federal income tax. But the threshold requirements are real: most advisors put the minimum viable candidate at 75 or more employees and $3M or more in EBITDA. Most small specialty contractors don't meet that bar.

Private equity and strategic buyers are where the external market data and the survey findings connect most directly. The 70% of owners who said they were seeing PE activity in their market are not wrong. Transjovan Capital reported an average PE multiple of 10.6x EV/EBITDA in construction deals, compared to 7.5x for strategic buyers. Those multiples are earned by companies with management depth, clean financials, and low customer concentration. A business dependent on its owner commands neither number.

Wind-down appeared in 10% of consideration responses — likely understated given the stigma it carries. For owner-operators where the business's value is genuinely inseparable from their personal involvement, a planned wind-down may be the most honest available path. It still requires planning: contracts to complete, retainage to collect, employees and GC partners to communicate with, and a personal financial picture that doesn't depend on a sale that may not materialize.

What the Survey Suggests Going Forward

The RiffleCM data points toward one finding that cuts across all the rest: 51% of trade business owners said a trusted advisor proactively raising the subject would most motivate them to start planning — ahead of reading an article, attending an event, or watching a peer go through an exit.

The planning gap is not primarily an information problem. It is a conversation problem. The data is available. What trade business owners appear to be waiting for is someone in their professional network to make the topic feel real and immediate.

The steps that close the gap are the same regardless of which exit path gets chosen: reduced owner dependency, cleaner financial records, personal savings outside the business, a realistic valuation. The thirty-point gap between owners who have thought about succession and owners who have a plan is not a gap in desire. It is a gap in the conditions that make planning possible.

For related reading: What Is Your Trade Business Actually Worth to a Buyer? and The Financial Dependence Trap: Why Trade Business Owners Can’t Afford to Stop Working.

Eliminating Manual Errors in Construction Bids

Common questions about reducing errors and improving accuracy

What causes most manual errors in subcontractor bids?

Manual errors usually come from disconnected workflows — things like outdated spreadsheets, inconsistent templates, or rekeying the same data multiple times. When project info lives across emails, texts, and PDFs, small mistakes add up fast.

How can software help reduce bidding mistakes?

Purpose-built estimating software automates repetitive tasks like data entry, quantity takeoffs, and revision tracking. Instead of chasing down the latest drawings or retyping costs, your team works from one centralized, accurate system — cutting errors before they happen.

Is automation complicated to set up for small subcontractors?

Not with modern tools like Riffle. You can connect your email or ITB inbox in minutes, and automation starts working behind the scenes — identifying bid invites, tracking updates, and helping you prioritize the right opportunities. No IT department required.

How much time can automation actually save?

Most subcontractors save 6–10 hours per week just by eliminating manual re-entry and version confusion. That’s more time for estimating the next job, reviewing margins, or simply getting home on time.

Does automating bids mean losing control over pricing?

Not at all. Automation handles the busywork — you keep full control over pricing, scope, and judgment calls. Think of it as an assistant that gets the numbers right so you can focus on strategy.

How do I know if my team is underspending or overspending on software?

A good rule of thumb: most subcontractors invest 1–3% of annual revenue in digital tools. If you’re still running bids manually or using outdated systems, the real cost might be hidden in lost time and missed opportunities.

Why does accuracy matter so much in bidding?

Every error compounds — one missed line item or miscalculated rate can erase your entire profit margin. Accuracy doesn’t just win jobs; it protects your business from losses you don’t see coming.

How does Riffle help subcontractors eliminate manual work?

Riffle automates your bidding and project workflows from start to finish. It finds ITBs in your inbox, organizes bid invites, fills in estimating data, and tracks updates — helping subcontractors bid smarter, reduce errors, and grow revenue.

We Understand the Bottlenecks for Subs

My biggest weakness has always been follow-ups—I’m just not great at it. If I had a built-in reminder feature to follow up on projects automatically, that would be a game-changer. I’ve gotten better, but I could still use that extra nudge.

Quoting can be chaotic. You have five different contractors sending out the same bid invite, each named differently. We end up with duplicate bids on the board or miss one entirely because it was labeled another way. There is no clear procedure when invites come in from multiple people.

Stay Informed

Get the latest on subcontractor business trends, research, and tools to help you grow profitably. Delivered monthly.